%20(3)%20(2).jpg)

Property crowdfunding and portfolio diversification

Portfolio diversification is a key principle for any investor to live by.

It simply means not putting all your investment eggs in one basket. In investment terms, it means allocating your investment funds strategically among different assets and asset classes to help manage risk.

If you put all your money into one company’s shares and they plunge, you’d lose your money. To take an extreme example, if at the start of last year, you had put all your savings into Carpetright shares, by the end of the year, you would have lost about nine tenths of the value of your investment. Weak consumer demand combined with restructuring made it a grim year for the company, which made a loss of £11.7m in the six months to the end of October, against a loss of £600,000 in the same period of 2017.

Similarly, if you put all of your money into a single bond and the issuer goes into insolvency, you could lose all your funds. Diversification is mitigating the risk by choosing different investments and types of investments. It doesn’t guarantee profits or protect against loss, but it may help protect your portfolio.

An effective portfolio diversification strategy is made up of different types of investments, called asset classes, which carry different levels of risk. The main asset classes are shares, bonds, cash, property and commodities. Each asset class tends to perform differently under similar market conditions, so splitting your assets among categories, helps to balance your portfolio. Investors typically choose a percentage they want to invest in each asset class based on their risk tolerance, years until retirement, and other factors.

In the UK, property has performed particularly well over recent decades and has proved to be a valuable element in many investors’ portfolios.

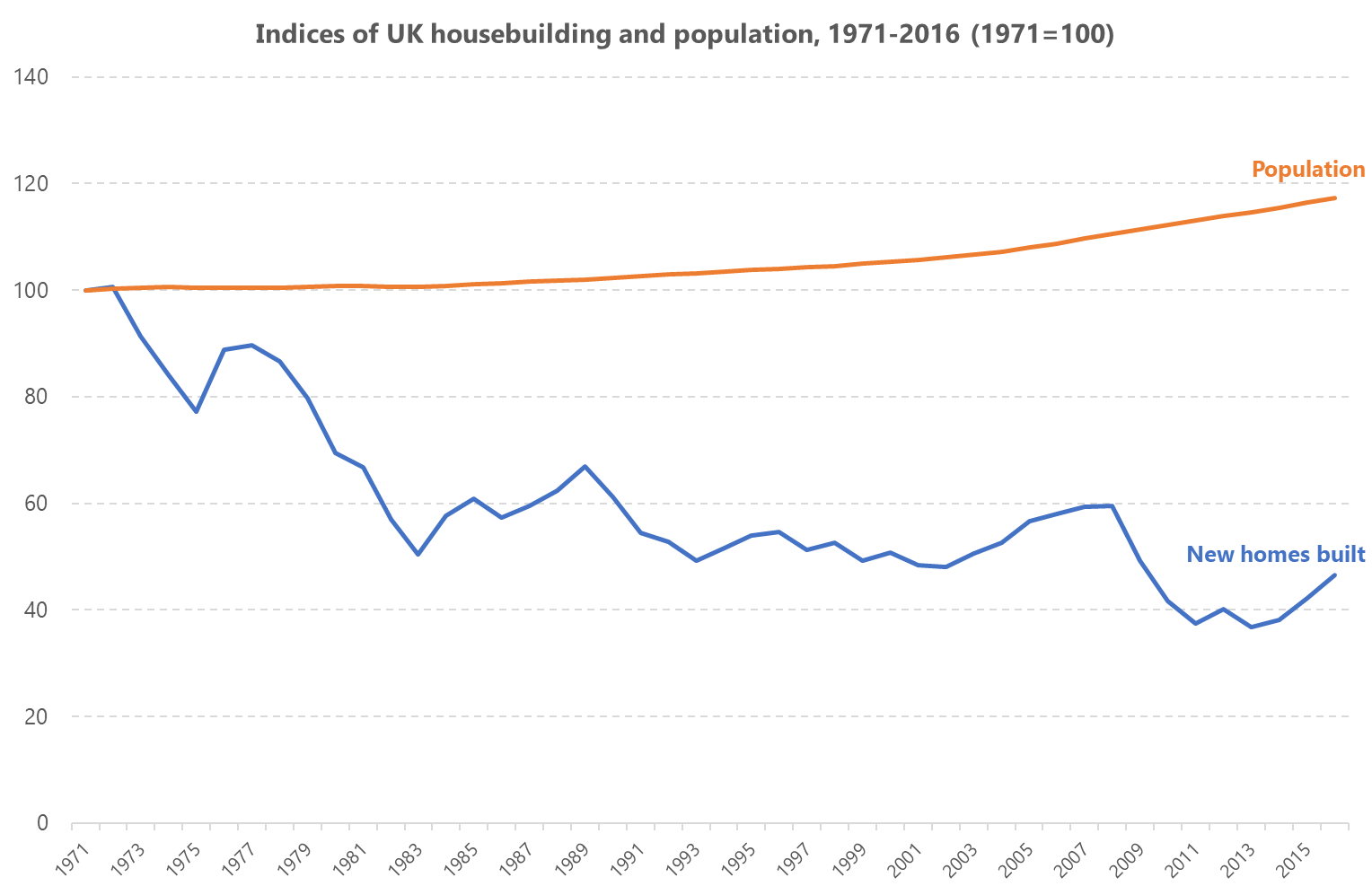

The UK has a rising population and a finite amount of land, which historically exerts an upward pressure on its value and therefore the value of homes built on it. The Department of Communities and Local Government records that the average UK house price in 1969 was £4,640. By 2007 this had risen to £223,405.

Add to that the fact that for some years the supply of new houses has failed to keep up with demand. It was calculated more than 10 years ago that at least 245,000 needed to be built in England every year to avoid a housing crisis. However in the following decade only 115,000 a year had been built. The economist and journalist, Liam Halligan, has pointed out that, over the past 30 years, the UK built about three million fewer homes fewer than required.

This has resulted in a housing crisis, which must put further upward pressure on prices and the property expert Savills predicts a total house price growth of 14.8% at a national level over the next five years in its autumn 2018 Residential Property Forecasts, Sure, there is considerable Brexit inspired uncertainty at the moment, but the property crash predicted in some quarters has failed to materialise and the housing market appears to be stable, with the exception of London, which has its own particular issues. Once Brexit is resolved, there is no obvious reason why housing and property values should not resume their historical trend.

So, it would seem that property investment should have a place in a diversified portfolio, the question is: what form should that investment take?

Until recently, the popular way into property investment was through buy-to-let. Only a year ago, the FT calculated that one in 30 adult Britons was a landlord, and that the rental income from buy-to-let properties, at an estimated worth of between £55bn and £65bn a year, was the equivalent to about 3% of national GDP.

The government came to the view that buy-to-let was distorting the market and introduced an additional 3% Stamp Duty charge for second homes. It also removed some of the tax reliefs available to property investors, and introducing new underwriting rules to make it harder for investors to raise the funds to finance property acquisition.

This has had a devastating effect on buy-to-let. A Residential Landlords Association survey in 2016 questioned 2,883 landlords and found that a no fewer than 58% were considering reducing investment in their property portfolios as a result of these changes and Savills found that mortgaged buy-to-let market purchases have fallen by 43%. The results of Belvoir’s Q3 rental index, compiled by TV property expert Kate Faulkner, also confirms that landlords are continuing to exit the property market.

Also a new report by Shawbrook Bank and the Centre for Economics and Business Research Activity forecasts the buy-to-let market dropping further in the next three years. The number of buy-to-let mortgages plunged in 2016 and 2017, falling from a multi-year high of 117,500 mortgages handed out in 2015 to 74,900 in 2017, a two-year drop of 36%.

An alternative to buy-to-let is simply to buy land and build a house or houses or to buy some property, improve it and then sell it for a profit. However, there is a problem with this approach when it comes to building a diversified portfolio and this also applies to buy-to-let. Basically, houses are expensive.

At the moment, the average UK house price is £226,906, so, if just one house, is going to represent the property asset class element of your portfolio, if that makes up, say 10% of that portfolio, that implies a pretty sizeable portfolio.

Even if that is attainable for you, it would still not represent truly balanced portfolio, because another principle of a diversification is diversification within asset classes. So with equities, the sensible investor would not just buy shares in one company – remember Carpetright? – but in different companies of different sizes, operating in different geographical markets and in different industries and sectors.

The same applies to property, but how to achieve that?

Enter property crowdfunding.

Online platforms have been developed which allow large numbers of investors to invest together through crowdfunding. These platforms bring the investor and investee together. Start-ups and start-up investors were among their earliest adopters. The property sector has followed, but in this case earnings are related to rental income and property value rather than business performance.

Property crowdfunding sites enable investment into specific developments through buying equity in a holding company that acquires a portfolio of rental properties. Also, there are peer-to-peer lending sites, which effectively loan money to individuals looking to acquire properties. In equity crowdfunding, the platform operator creates a separate company for each investable opportunity.

There are a number of advantages to property crowdfunding. The investor’s risks are reduced, because exposure is limited to the amount invested and the original investment would be secured against the value of the land purchased. There is also the potential for good returns. The amount returned to investors is a percentage of the profit achieved equal to the proportion of equity held. If, for example, someone invests £5,000 for 1% of the shares in a small development and that development makes a profit of £250,000, then the investor will be entitled to a 1% share of that profit, or £2,500, along with repayment of his original £5,000 investment.

And one of the major benefits is that it allows the investor to build up a diversified portfolio of property assets. It’s possible to buy shares in a property development through crowdfunding for as little as £100. This allows the investor to spread his investment among different platforms, different developers, different types of property and in different parts of the country.

Furthermore, with the typical length of a development project being between 18 months and two years, the investor has the flexibility of being able to regularly adjust the balance of their investments.

Portfolio diversification is a need and property crowdfunding helps to meet that need.